Advices on instant loans

Summary

The truth about instant loans

- Instant loans are a growing industry in Québec. Even though new legislation has been passed to regulate them, some lenders still use questionable practices.

- Instant loans offer money that appears easy to borrow but actually comes with very high interest rates. As a result, they can be very difficult to pay back.

- This isn’t the type of loan you can use to improve your credit score. In fact, banks are often wary of clients that have previously taken out instant loans.

When you’ve hit a financial snag, it’s only natural to look for the easiest solutions. That’s often when you might start noticing ads for instant loans that promise easy money without a credit check. It may sound appealing, but do you know the truth behind this kind of financing?

How do I recognize instant loans?

A growing number of businesses in Québec specialize in “instant” or “payday” loans. They are anything but subtle. Their marketing includes flashy ads and brightly coloured posters. “Easy cash in 1 hour,” “No credit check,” “Express loans”: you’ve surely seen this kind of slogan before.

Instant money lenders offer small loans of a few hundred dollars that they deposit directly into your account without running a credit check or asking you to provide any documents. It’s a very quick process. Goodbye waiting, hello quick money!

It really does sound too good to be true. That’s because fast cash comes at a steep price.

Who are instant loans for?

Instant loans are obviously aimed at people who don’t want to share their credit scores because they aren’t very good. These people often have a lot of debt, tend to make late payments, or have filed for bankruptcy or a consumer proposal.

They know that if lenders check their credit score they’ll be considered a “risky” borrower. For these borrowers, instant loans are a last resort.

How do they work?

Instant loans count as private loans. You provide certain personal information (like your social insurance number, a pay stub or a bank account number), and are granted a loan.

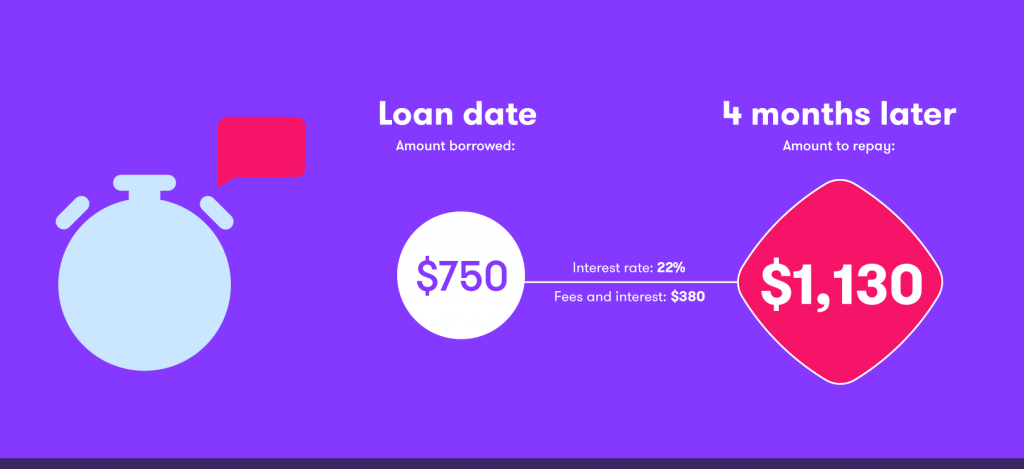

These are loans for smaller amounts, usually between $250 and $1,250, but some lenders offer up to $5,000. So these lenders generally don’t offer large loans. The interest rates, however, are sky high. They can reach up to 29%! You also don’t have a long time to pay the loan back: frequently less than a year.

What are the disadvantages of an instant loan?

The high interest rates can cause your debt to snowball. And that’s not including unexpected “transaction fees” that may be tacked on. Here’s what this could mean for your wallet.

Example of an instant loan

That said, new regulations for high-cost credit contracts were added to the Consumer Protection Act in 2017 to better protect consumers. The Act now requires that lenders check whether you actually have the capacity to pay before giving you a loan.

Is it as risky as people say?

As mentioned above, instant loans can dig you deeper into debt. They can also come with some unwanted surprises. In the past, lenders have been accused of using bad practices like misleading ads that make no mention of the very strict repayment conditions and exorbitant interest rates. Companies have also been caught charging hidden fees and even carrying out their activities without a permit.

If I’m careful, are there any advantages?

If you are expecting to improve your credit score with an instant loan, you’ll be disappointed. Even if you pay it back on time. That’s simply because this type of loan has little to no influence on your payment reputation. Often banks are even wary of clients who use this type of financing.

The biggest disadvantage of instant loans is that they’re expensive. They work in a way that guarantees you’ll pay a lot more than you’ve borrowed.

Are there alternatives to instant loans?

Struggling to make ends meet is stressful, and it’s normal to look for an emergency exit. But before considering an instant loan, go over your budget. If your financial problems seem insurmountable, seek assistance.

Have you already thought about talking to a counsellor in financial recovery? These experts can help you find a way out. Their role is to look at your budget and suggest the best options for you. Sure, it’s not as quick as an instant loan. But it’s also a longer-term solution.